Associated Companies

Please note that this article does not address issues relating to groups of companies. Please contact us directly to discuss Corporation Tax for groups.

What is an associated company?

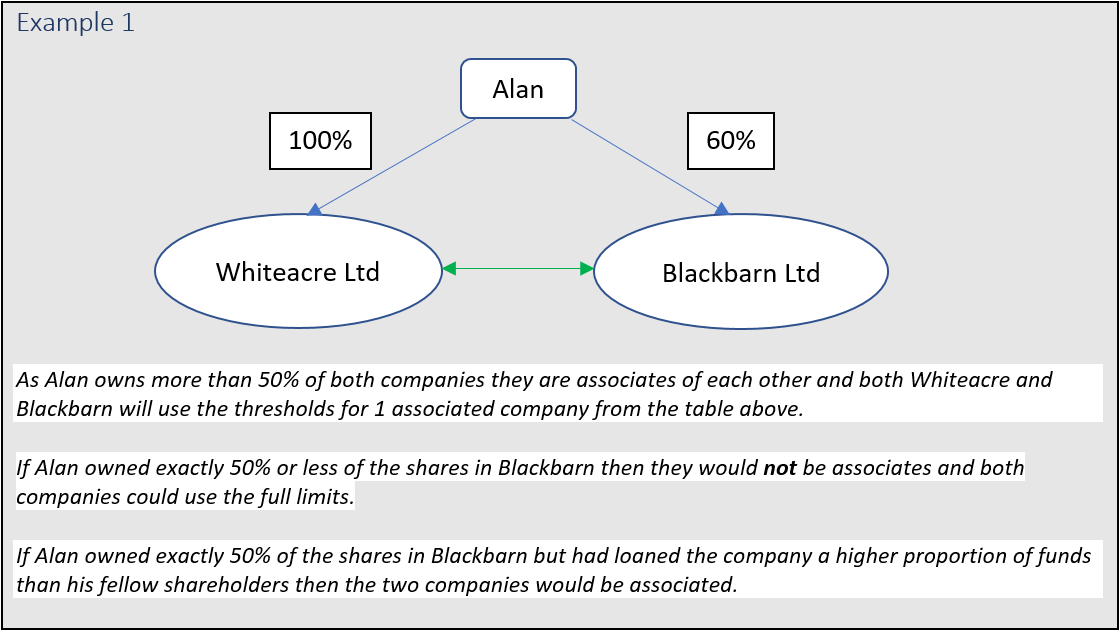

A company is associated with another company where they are controlled by the same person or persons. This is sometimes referred to as “companies under common control”.

What does this affect?

The two main impacts of the number of associated companies are a reduction in the profit limits for the rate of Corporation Tax payable, and a reduction the profit level at which Corporation Tax is payable by instalments.

| Number of associates | 0 | 1 | 2 | 3 |

| Corporation Tax Lower Limit |

£50,000 | £25,000 | £16,667 | £12,500 |

| Corporation Tax Upper Limit |

£250,000 | £125,000 | £83,333 | £62,500 |

| Payment by instalments | £1,500,000 | £750,000 | £500,000 | £375,000 |

Profits up to the lower limit are taxed at 19%, profits above the upper Limit are taxed at 25% and profits between these levels are taxed at a marginal rate of 26.5%.

What is meant by control?

Control will usually mean owning more than 50% of the Ordinary or voting shares in a company, however a company can also be controlled via loans or a combination of shares and loans.

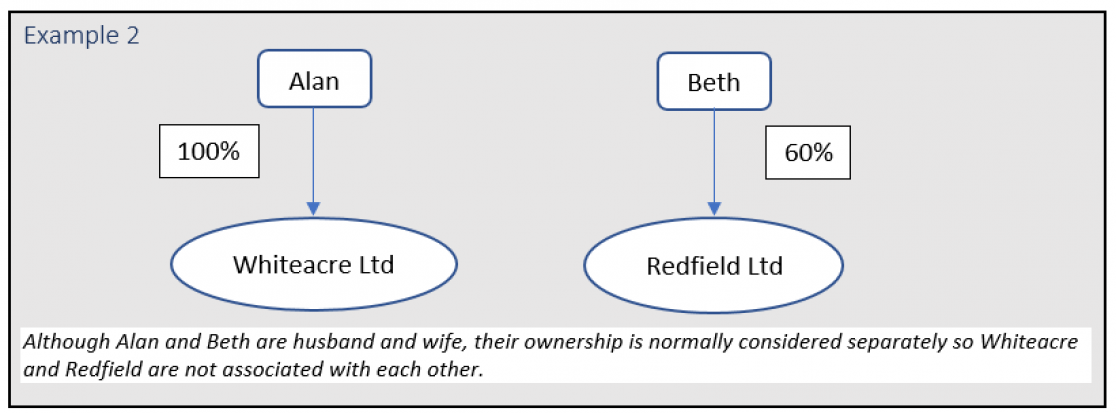

What about companies owned by family members?

In most cases companies controlled by individual family members will not be associated with each other – see example 2.

However, family members shareholdings can be combined where there are sufficient links between the companies in any one of three categories:

- Financial links - loans or investment in joint projects

- Organisational links – sharing of staff or premises

- Economic links – where both businesses have the same customers

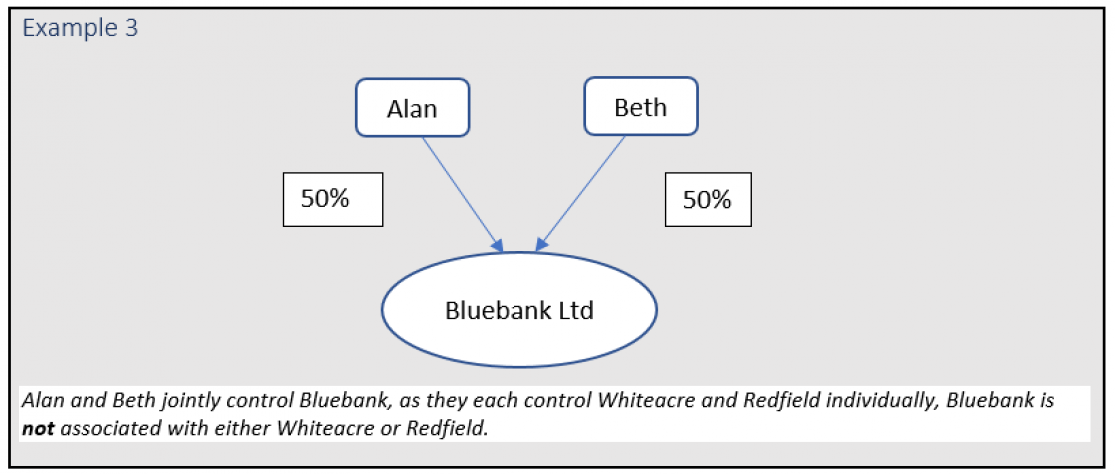

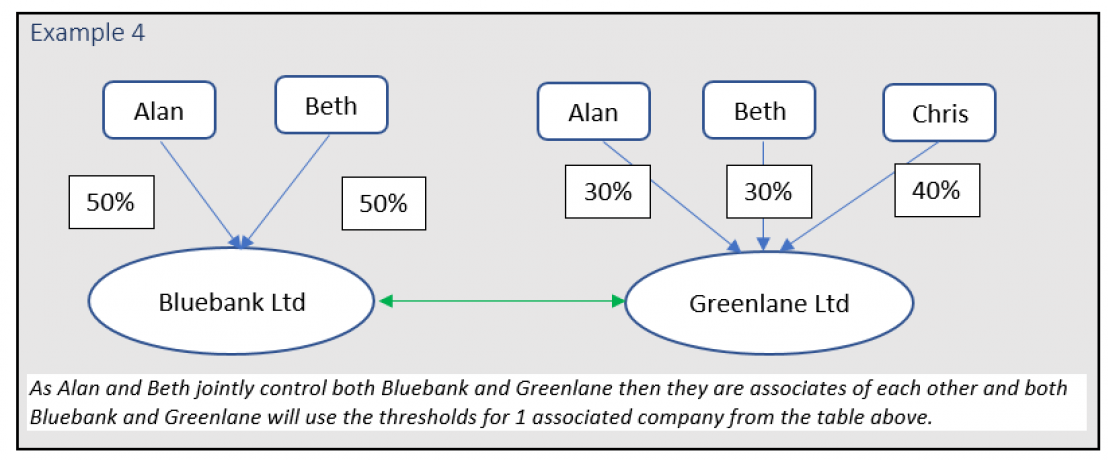

How does this work when there is more than one owner?

Where a company has more than one shareholder and no single shareholder is in control, then the number of associated companies are worked out by looking at which combinations of shareholders can control the company.

As these rules will affect each business differently, please contact us if you would like to know how these rules will impact you.

Disclaimer: The information contained in this note is of a general nature and is not a substitute for professional advice. Please speak to us to obtain specific professional advice before you take any action. No responsibility for loss to any person acting or refraining from action as a result of this budget note is accepted.

Posted on 6th February 2023 by Joe Attwood.